For brokers looking to bolster revenue during the market dip, premium funding can attract clients in need of cover.

by Elana Benjamin

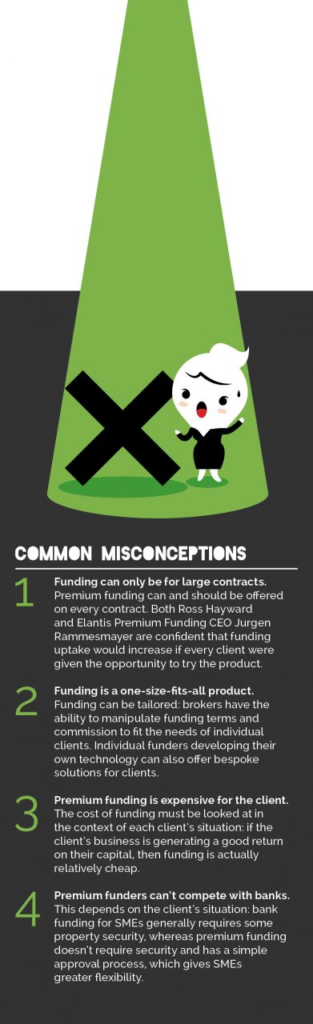

“Premium funding is probably the easiest form of finance you can get,” says Premium Funding Director Ross Hayward.

But according to Premium Funding’s September 2015 White Paper and Broker Survey, only 36% of brokers automatically offer all clients a funding option.

In the current market – with insurers aggressively competing for business, nose-diving premiums and reduced broker revenue – premium funding is a relatively simple way for brokers to generate extra income.

So how can brokers become more sophisticated users of premium funding and increase its take-up?

THE BASICS

Premium funding is a point-of-sale product that allows businesses to pay their insurance premiums in regular installments instead of all at once.

Premium funding isn’t intended for situations where clients can’t afford their insurance. Rather, it’s a cash flow solution; a form of finance that frees up money for other expenses in a client’s business.

Aside from cash flow management, premium funding has other benefits for insureds. It’s a low-cost form of finance that’s unlikely to affect existing loan covenants.

The rates are extremely competitive compared to other forms of financing and it is debt without personal guarantees, or charges over business or assets.

For brokers, premium funding can provide a valuable alternative revenue stream. Although the average broker commission is around 2.5%, the percentage of broker commission varies depending on the value of the funding contract and the length of the loan.

Generally, the longer the funding contract, the lower the broker commission; longer funding contracts lead to higher interest, with brokers lowering their commission to make funding more palatable to the client.

In Australia, approximately 30% of commercial policies are funded. In 2014, Insurance Premium Financiers of Australia (IPFA) – an industry body comprised of 13 premium funders, mostly non-bank – funded a total of $4.8 billion worth of premiums.

The vast majority was the funding of commercial insurance policies, with the average commercial premium being funded worth just $17,910. Indeed, Elantis Premium Funding CEO Jurgen Rammesmayer says the majority of businesses with premium funding are SME-sized.

Although funding is utilised across a broad range of industries, Premium Funding’s White Paper reported that funding is used most by the manufacturing, construction and retail industries. But if brokers were to send out funding contracts with all new business and policy renewals – irrespective of premium size – this mix could change.

FEELING THE SQUEEZE

The premium funding sector is directly affected by the insurance market. Since funding is calculated as a percentage of total premium, the current soft market is squeezing the industry.

Between 2013 and 2014, the amount of premium funded by IPFA members fell $300 million, to $4.8 billion. Rammesmayer predicts the amount of premium funded in 2015 will be even less.

Contributing to this is the trend towards insurers offering pay-by-the month facilities and clients using either cash reserves or bank finance to fund their premiums.

Bigger companies, which tend to have more expensive premiums, generally have greater flexibility as to how they fund their insurance premiums.

“With the availability of credit in the market and the decrease in lending rates over the past two years, we’ve seen an increased number of these larger clients choosing bank lending over premium funding,” Rammesmayer says.

“With interest rates being so low, a funding line from a bank can sometimes be cheaper than premium funding. That’s because premium funding rates haven’t come down as much as bank lending rates, since the average broker commission hasn’t changed.”

But Rammesmayer says brokers are starting to recognise this shift and respond by reducing their commissions, especially where their clients have alternative funding options.

Similarly, Premium Funding’s White Paper reported that the percentage of quotes converted to funding contracts is decreasing across all contract values.

The most marked decrease in conversion was reported within the $50,000 to $100,000 contract value: in 2013, 60% of quotes in this range were funded, but only 42% were funded in 2015.

The explanation for reduced conversions? With the low cash rate, more clients are looking to pay their premiums outright due to high cash reserves.

STRENGTHENING THE BOND

With Premium Funding’s Broker Survey finding that only 57% of brokers view premium funding as ‘a strategic tool to grow income and retain business’, there’s clearly scope for brokers and premium funders to work more collaboratively to win extra business.

Premium Funding’s White Paper has one clear bit of advice for brokers on this front: “In this new competitive landscape of insurance, you need to have a panel of good funding options, products and people so you’ve got every chance of winning every client that comes into your office.”

It’s also worth remembering that providing funding options to clients isn’t just about generating broker revenue. It’s also about strengthening the broker-client relationship and positioning the broker as a partner in their client’s business.

In an age where digital platforms are disrupting traditional ways of placing insurance business – and transforming the broker role – being able to add value like this is imperative.