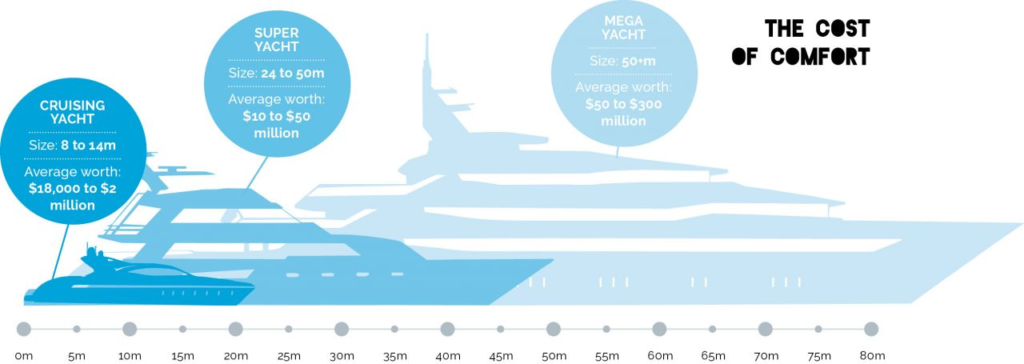

Private yachts are as unique as their cashed-up owners and need insurance tailored to cover bespoke equipment, vast regions and uses that most brokers can only dream about.

by Steven Chong

Rupert Murdoch’s Rosehearty had pale-oak furniture upholstered in Hermès leather and a jacuzzi, but Vertigo has got an extra 10 metres and electrochromic glass panels. Lachlan and Sarah Murdoch have the 42.6 metrecarbon-fibre Sarissa. Marcus Blackmore recently sold 150,000 Blackmores shares – they’ve since trebled in value to $150 – to buy a seventh to go with his Squirrel jet-engine helicopter.

As with clothing or cars, at the apex of the boat market utilitarian mass production yields to the time-honoured traditions of haute design, bespoke craftsmanship, specialised fittings, tailored enhancements and opulent extras à la carte. The resulting product may be unique and of a high net value, and, without skilled seamanship or maintenance, is likely vulnerable to depreciation due to maritime risks as dynamic as the elements.

But insurance is almost as old as seafaring itself and a vibrant Australian market has evolved to tailor luxury vessel cover. As an island nation with more than its fair share of plutocrats floating in and out, Australian brokers are particularly well-placed to specialise in this market.

Trident Insurance Marine Manager Stephanie Muller says there is much to consider when insuring a luxury vessel that can traverse the globe for months on end, but it’s a common misconception that it’s hard to understand. “It’s not rocket science, nor dissimilar to the information required to insure the client’s vehicles. We make every effort to make the whole process as simple and easy to understand as possible and encourage our broking partners to let us explain the product,” Muller says.

Customised policies are generally more flexible than ‘off the shelf’ products and Muller says the following features are advantageous:

New for old replacement – this is the basis of settlement, rather than agreed or market value. “The cost the owner forgoes on maintenance and care of their pride and joy, in terms of time and money, is enormous. The policy should respect that,” Muller says.

Cover for paid crew – general policies do not usually provide this, but would be relevant if the boat leaves

Australian waters.

Tender and personal water craft (PWC) – regular policies will cover a tender for the vessel, whereas a superyacht package can cover several and also PWCs, such as jet skis.

Vessel use – cover can extend beyond private use so that personal or corporate entertaining, occasional charter and exhibition in boat shows can also be covered.

When the owner plans to venture outside of Australian waters, Muller advises brokers to seek a cruising itinerary, which may be subject to change, and quote accordingly.

LESSONS IN LIABILITY

Nautilus Marine Insurance Director and CEO Lyndon Turner says that standard policies tend to be found wanting when it comes to territorial provisions because they commonly omit limits within states, or disregard the fact that some territories exclude common boating activities, like on-board fishing, water-skiing, diving equipment or even a trailer boat.

“Take care to explain the liability components of the policy so that personal injury to third parties is automatically covered in addition to third-party property,” Turner says. “Owners can also be liable in some jurisdictions for pollutants released from their boat in the event of damage, so should as standard include pollution and environmental protection.”

An insurance broker edging into the luxury pleasurecraft space should get a good handle on their client’s requirements. “It’s a duty-of-disclosure environment where you have to work closely with the client to determine insurance needs based on how they intend to use the vessel.

This leads to how their risks determine the appropriate customisation,” Turner says.

Turner says that getting the basic cover and excess structures right are fundamental. He recommends insuring on an agreed-value basis and not market value because it is subject to significant variation.

“Plus, some wordings don’t have clear excess structures that can include set depreciation and very important for all clients is the requirement to ensure regular proactive maintenance to maintain seaworthiness,” he says.

Furthermore, specialist advice helps ensure that cover is well-placed and economic. “Leveraging specialist expertise helps to decide what needs improvement and continual investment,” Turner says.

“Nautilus underwriters are not surveyors or repairers, but sit on industry boards and try to stay equally close to both boating and insurance, and support brokers with advice via checklists and expert written articles on vessel ownership and maintenance.”

POLICY PACKAGING

For Trident Insurance’s Stephanie Muller, fostering the broker-owner relationship is key to anticipating risks.

“Your client will generally be happy to chat about their boating life to date – you’ll be gathering important info for your insurer plus building a rapport with the client. What it’s made of, what year it was built, its home port and cruising range are all important factors,” Muller says.

However, Muller warns, brokers can sometimes underestimate the importance of marine cover, especially for clients with big budgets.

“The most common mistake brokers should avoid is to presume their client’s boat is just a small ‘add-on’ to an account and not something to spend much time on,” Muller says.

“But it’s important to them. It’s where they spend their hard-earned leisure time and they definitely want the best cover. Major accounts are won and lost on the handling of the insurance of ‘the boat’.”