Last week’s tragic fire at London’s Grenfell Tower has again raised the profile of the risks of flammable building cladding and brokers are being advised to be vigilant when assessing building risks.

Reports indicate that the cheap cladding used on the outside of the London tower block fuelled the fire now believed to have killed nearly 60 people.

Indeed, perhaps inexcusably, incidents such as this could have been prevented, as it certainly wasn’t the first building to suffer the effects of the substandard cladding. In July last year, Dubai Marina’s 75-storey Sulafa Tower went up in flames, following several similar fires in the Middle East, including one at the 63-storey The Address Downtown Dubai on New Year’s Eve 2015.

Of course, here in Australia, there was Melbourne’s Docklands Lacrosse apartment fire in November 2014. And it wasn’t until January 2017 that the owners of the building were required by the Building Appeals Board to remove the rest of the material, according to The Age. It quashed a bid by LU Simon Builders to keep the cladding and instead install more sprinklers, saying the equipment might fail with “catastrophic” results.

NIBA has previously reported on policy issues with cladding in February last year, noting that following the Docklands apartment building fire, the Victorian Building Authority was prompted to audit 170 buildings as part of their investigation. The audit found 51 per cent of the buildings were non-compliant.

Reports have since emerged that Australia’s cladding problem is not confined to Melbourne, and it’s expected there will be a large flow-on effect for the insurance industry.

As such, brokers are being advised to exercise vigilance and seek out whether a building they’ve risk assessed contains the aluminium composite panels (ACP), and if so, are they compliant?

Speaking to IRP in February 2016, Andrew Nock Valuers founder Andrew Nock sagely advised brokers to “go back to the builder, seek the checklist of all goods used in the building construction of the actual building, and then make sure that none of that cladding from China was used on their buildings. It’s Australia wide now”.

Over the weekend, ABC News reported that the NSW Government is considering tougher regulations on the use of combustible cladding in the wake of the deadly Grenfell Tower fire.

Alarmingly, State Government documents have warned up to 2,500 buildings in NSW could be fitted with flammable cladding.

“We have been working very hard behind the scenes since the tragedy in London,” Premier Gladys Berejiklian said.

Helen Napier, previously of Zurich Australia and Canegrowers, now Regional Manager – Queensland of the NAS/Westcourt network, has experience with cladding fire issues from her previous roles, and now works to educate the network on best practice risk management in this area.

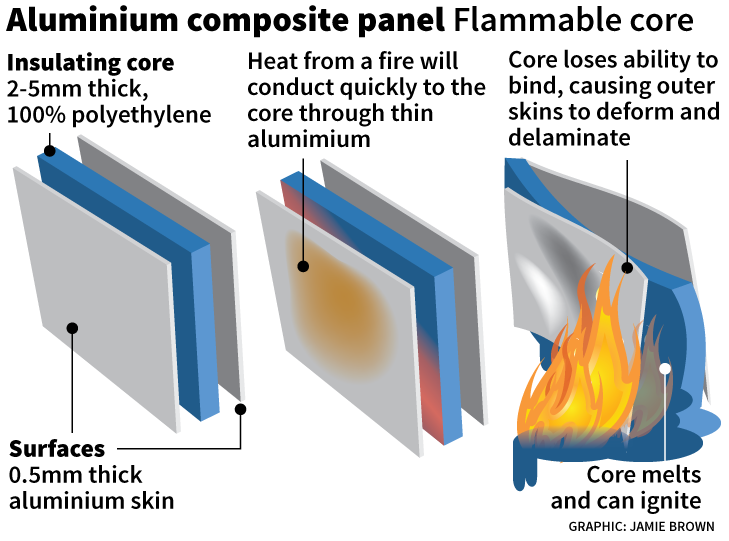

“These panels are lightweight, easy to install, and provide an attractive metallic building finish. The panels typically range from 4 to 6 mm in thickness, made up of two outer aluminium skins, separated by an inner insulating core. Unfortunately, the most common core material used in these panels is highly combustible polyethylene (PE) plastic! There are also fire-rated ACP cladding panels which have a mineral core, but there has been a lot of imported, lower-cost, non-fire-rated material used in the industry. It’s hard to tell the difference between the panels unless samples are taken and tested. If there is information on the exact product used this is also very helpful.”

Previously, Napier noted that not all underwriters ask the question on their electronic platforms – there is not always mention in the drop-down box of ACP, so it could fly under the radar. They will ask about EPS, as that was a more well-known material risk, but not ACP – this might now change.

“The fire, as terrible as it is, has made it a well-known topic and likely to be included in fact finders going forward. The issues have been that owners don’t always know what kind of material their buildings contain, so they just say ‘metal’,” Napier notes. “Brokers need to dig deeper and ensure they know what kind of metal. If they say aluminium panels – you need to ask for the brand and provide any specifications, then refer it to the insurer and ask for their guidance – they will consult their risk engineer.

“More care needs to and should be taken. Construction of a building is a material fact – if a party (the client or the broker) knows the building is constructed of ACP, they have the responsibility and obligation to declare this, and it is our job as a broker to find out more information to confirm if the panels are compliant or not. We are obliged to ensure the right questions and answers are ascertained,” added Napier.